November 8, 2017 | Katherine Blakeley

Shifts in the international security environment, as well as calls by the Trump administration for a “historic” defense increase, have led analysts, Congressional leaders, and senior Pentagon officials to hope for or expect a defense buildup commensurate with the Reagan-era buildup of FY 1979–FY 1985. Secretary of Defense James Mattis and House Armed Services Committee Chairman Mac Thornberry (R-TX) have called for, at a minimum, sustained 5 percent annual increases to the defense budget above the FY 2018 request.[1] Chairman of the Joint Chiefs of Staff Joseph Dunford stated in testimony that the capabilities to support the forthcoming National Defense Strategy would require the defense budget to grow by between 3 and 7 percent annually through FY 2023. Even so, this increased level of funding would not allow the military to increase the size of the force.[2] Analysts are banking on 4–6 percent annual growth in procurement funding, down from more aggressive expectations of high single-digit or low double-digit growth espoused shortly after the election in 2016.[3] Although there are some important parallels between the early 1980s and today, there are also some critical differences that make an equivalent defense buildup less likely to occur.

First, defense spending is shaped by the perceived demands of our national security in a shifting and challenging international security environment filtered through political considerations; it should not be an arbitrary round number or percent of GDP. The Reagan-era buildup occurred in against the background of broad bipartisan perception of an increasingly unfavorable U.S. position in its bipolar strategic competition with the USSR. By contrast, national security practitioners and policymakers have only recently begun to recognize the current shift from the unipolar security environment of the post-Cold War era to an era of renewed competition with Russia and China, as well as other challenges to the U.S.-led international order, and there is as yet no consensus as to its key features.[4]

Accordingly, there is not yet a shared understanding of the types of military strategies and capabilities that will be most important to the United States in this increasingly challenging environment. Decisions about what investments in military capabilities may be needed (for example, a more robust U.S. military and allied presence in Eastern Europe with heavy brigades, ground-based fires, greater airpower, and capabilities to operate in a high-end contested combat environment) or the appropriate balance between high- and low-end capabilities in the Air Force and Navy, and therefore the level of defense spending that may be required, should be grounded in a clear vision of the international security environment, U.S. objectives, and the role of our allies and partners. Additionally, this epochal shift in the international security environment demands a corresponding focus on longer-term thinking about U.S. strategy, capabilities, and defense budgets, struggling against the tyranny of immediacy imposed by national security crises, domestic political calculations, and near-term bureaucratic victories in the budget process.

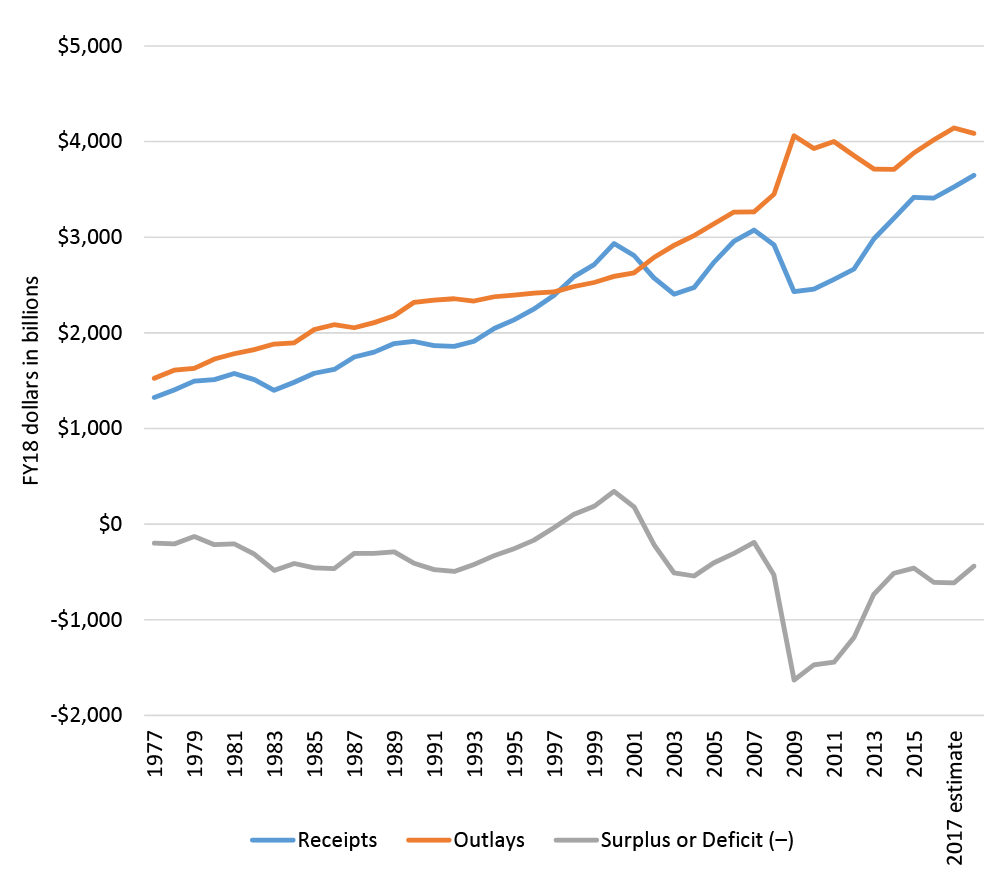

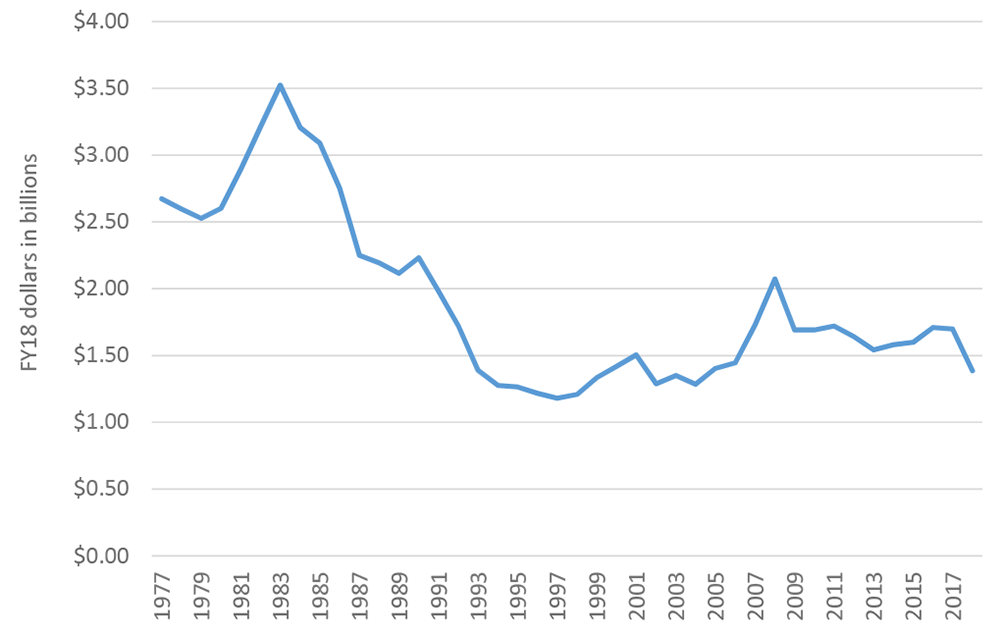

Secondly, the contemporary defense spending budgetary landscape is very different than it was during the Reagan-era buildup. The rapidly increasing defense budgets of FY 1979–FY 1985 were financed predominantly through deficit spending, as the Reagan administration cut taxes in 1981, decreasing revenues in both absolute and relative terms (see Figure 9-1).[5] The rapid growth of the deficit and rising outlays led to the enactment of the Gramm-Rudman-Hollings Balanced Budget Act of 1985. This law, the grandfather of the current Budget Control Act of 2011, imposed caps on overall discretionary spending levels in an attempt to reduce the federal deficit. The Gramm-Rudman-Hollings Act effectively halted the Reagan administration’s defense buildup, and defense spending contracted rapidly after the FY 1985 high water mark. By contrast, the contemporary BCA is already in force, and has placed caps on defense and non-defense spending through FY 2021 that are enforced by the sequester mechanism borrowed from the Gramm-Rudman-Hollings Act, smothering a prospective defense buildup. Although Congress has reached a bipartisan deal to amend the defense caps each year since FY 2013, the average amount of so-called sequester relief has been $18 billion in FY 2018 dollars, reflecting the narrow boundaries for compromise between the fiscal hawks, mainline Republicans, and Democrats. Without an agreement to substantially raise or eliminate the BCA caps, any growth in defense spending will be far below a comparable buildup in either total amounts or rate of growth.

Figure 9-1: Federal Receipts, Outlays, and Surplus or Deficit, FY77–FY18

Source: OMB, Historical Tables, Budget of the United States Government, Fiscal Year 2018 (Washington, DC: Government Printing Office, 2017), Table 1.3, “Summary of Receipts, Outlays, and Surpluses or Deficits (-) in Current Dollars, Constant (FY 2009) Dollars, and as Percentages of GDP: 1940–2022,” available at https://www.whitehouse.gov/sites/whitehouse.gov/files/omb/budget/fy2018/hist01z3.xls. Calculations by CSBA.

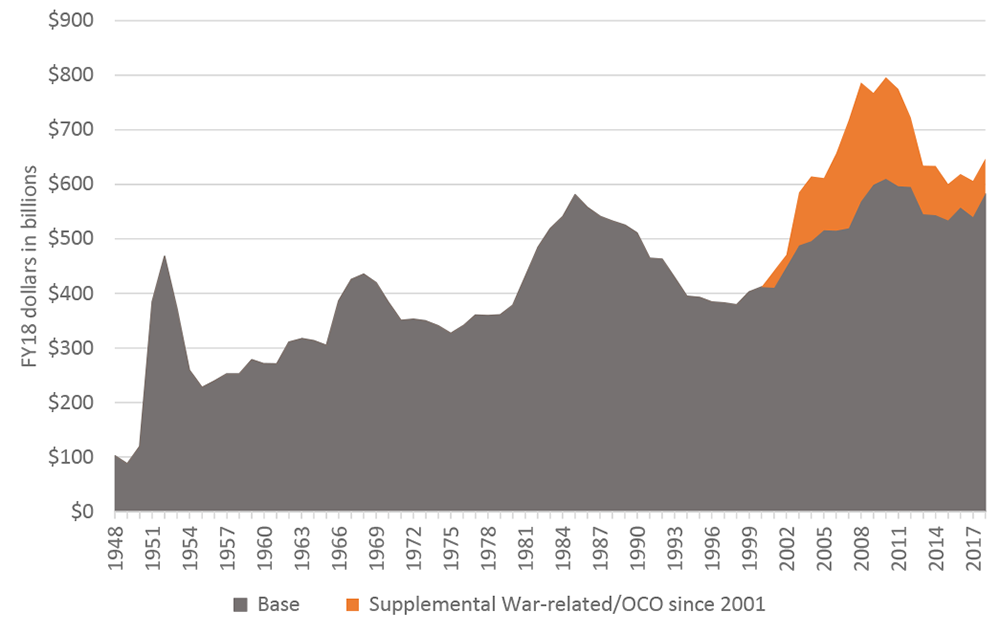

Third, total DoD budgets have exceeded those of the Reagan-era defense buildup since FY 2003, prompting some to ask why even higher defense spending is justified and what we’re collectively getting from our national spending on defense. In an annual Gallup survey for 2017, 31 percent of Americans surveyed felt that the U.S. was spending “too much” on defense.[6] The FY 2018 DoD budget request of $647 billion (including base, OCO, and mandatory spending) is $65 billion, or 11 percent, more than the $581 billion defense budget at the peak of the Reagan buildup. Even excluding Overseas Contingency Operations funding, the base defense budget request still matches or exceeds the average funding levels of the Reagan-era buildup after adjusting for inflation. The FY 2018 base budget request of $582 billion (including both discretionary and mandatory spending) is slightly higher than the peak of the Reagan buildup of $581 billion in FY 1985 and $59 billion, or 11 percent, more than the average DoD budget of $523 billion during the Reagan Administration.

DoD’s largest total budget, at $796 billion, was in FY 2010 during the height of the wars in Iraq and Afghanistan. It included $610 billion in base defense spending—$29 billion more than the $581 billon at the peak of the Reagan-era buildup—as well as an additional $186 billion in OCO funding. Defense spending declined rapidly following the drawdown of deployed forces in Iraq and Afghanistan and the imposition of caps on base discretionary defense spending by the Budget Control Act (BCA) of 2011. Despite the decline, total national defense funding at the bottom of the drawdown in FY 2015 was $628.9 billion, $32 billion more than the $596.9 billion spent on national defense during the peak of the Reagan-era defense buildup, after adjusting for inflation. The base defense budget in FY 2015, at $534 billion, was $11 billion or 2 percent more than the average base defense budget level during the Reagan-era buildup, although it remained below the peak base budget of $581 billion in FY 1985 by $47 billion (see Figure 9-2).

Figure 9-2: Total DOD Base and OCO Spending, FY48–FY18

Source: OUSD (Comptroller), National Defense Budget Estimates for FY 2018, FY 2018 Greenbook (Washington, DC: DoD, June 2017). Calculations by CSBA.

Overall, the share of defense spending as a percentage of GDP has declined steadily since the end of the Korean War. The U.S. national GDP grew from $2.27 trillion in FY 1948 to an estimated $20.0 trillion in FY 2018 in constant dollars—a cumulative annual growth rate (CAGR) of 3.2 percent. Over the same time period, defense spending has risen from $102 billion in FY 1948 to a requested $646 billion in FY 2018 for a CAGR of 2.7 percent (see Figure 9-4 and Figure 9-5). Although total defense spending over the past 15 years has reached historic highs in absolute terms, it represents a historically low percentage of GDP. Although not useful for gauging the necessity of defense spending, defense spending as a percentage of GDP or as a percentage of overall federal spending can be a useful yardstick in discussing the relative affordability of spending on defense—or any other federal program. Spending a lower percentage of GDP on defense indicates that national security consumes a relatively small proportion of overall national economic activity, compared to the FY1979–FY 1985 defense buildup. Similarly, defense spending’s relatively low share of federal spending in historical terms indicates that more money could be allocated to defense, if the political will to do so existed.

Funding for the Department of Defense peaked at 30 percent of federal spending in FY 1983–FY 1985, when it was equivalent to 6.7 percent of GDP (see Figure 9-3). In FY 2017, defense outlays were $581 billion, higher than outlays during the peak of the FY 1979–FY1985 buildup, but defense spending was a much lower 14 percent of federal spending and 3 percent of GDP. From an overall affordability perspective, the nation could increase spending on national defense considerably in dollar terms, while remaining below past proportions of defense spending as a share of GDP or federal spending. Spending the equivalent of 6.7 percent of GDP on the Department of Defense in FY 2018 would result in a DoD budget of $1,341 billion, while allocating 30 percent of federal spending to the DoD would result in a budget of $1,228 billion. This would be an increase of $459 to $534 billion over the total FY 2018 DoD request of $647.

Figure 9-3: Defense Spending in Absolute and Relative Terms, FY77–FY18

Source: OUSD, FY 2018 Greenbook. Calculations by CSBA.

Figure 9-4: GDP, Federal Spending, and DOD Budgets

Source: OUSD, FY 2018 Greenbook. Calculations by CSBA.

Figure 9-5: DOD Budgets as a Percentage of Federal Spending and GDP

Source: OUSD, FY 2018 Greenbook. Calculations by CSBA.

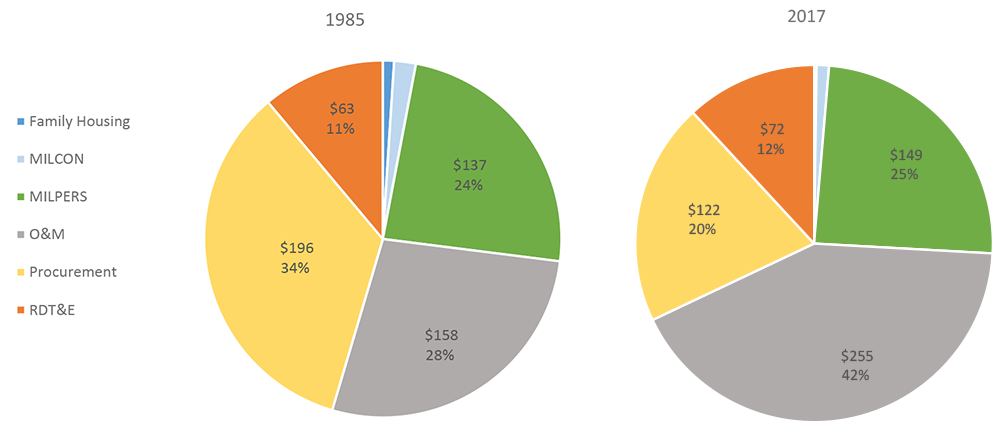

Beyond the topline figures, a dollar of defense funding in the 1980s was spent much differently than a dollar of the defense budget today. Accordingly, even an equivalent expenditure would not yield an equivalent force structure. At the peak of the Reagan-era defense buildup in FY 1985, the Pentagon was spending 34 percent of its budget on procurement and 11 percent on RDT&E, for a total of 45 percent on what is often termed “modernization.” By contrast, modernization only received 32 percent of defense spending in FY 2017, with procurement accounting for 20 percent and RDT&E 12 percent. After adjusting for inflation, procurement spending was $196 billion in FY 1985, but just $122 billion in FY 2017—38 percent less (see Figure 9-6 and Figure 9-7).

Figure 9-6: Defense Spending by Appropriations Title, FY85 and FY17, in FY18 Dollars

Source: OUSD, FY 2018 Greenbook. Calculations by CSBA.

Figure 9-7: Composition of Defense Budget in FY85 and FY17 by Appropriations Title

Source: OUSD, FY 2018 Greenbook. Calculations by CSBA.

Note: FY 2018 dollars in billions.

Figure 9-8: Ratio of Procurement vs RDT&E Funding

Source: OUSD, FY 2018 Greenbook. Calculations by CSBA.

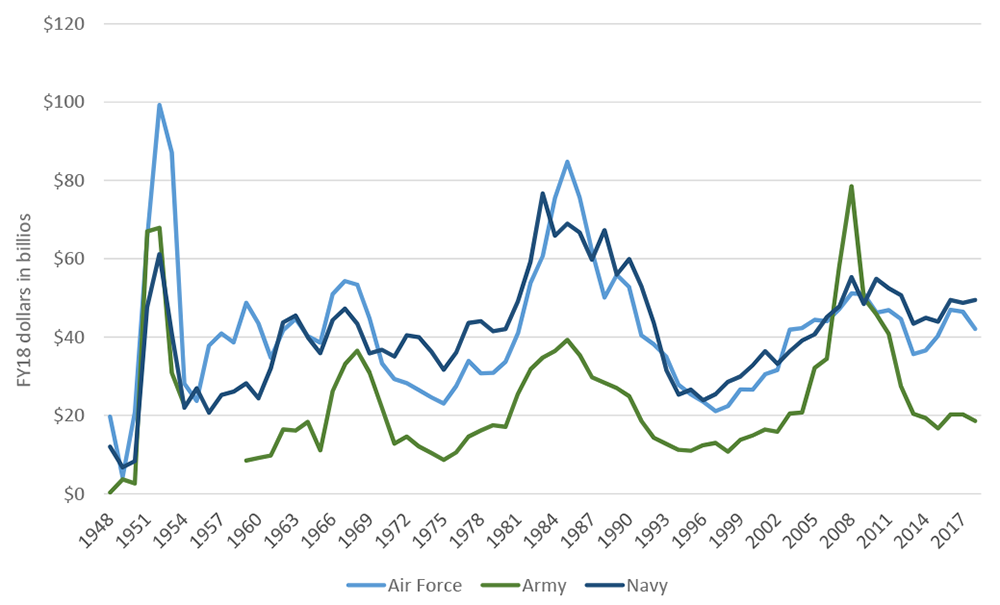

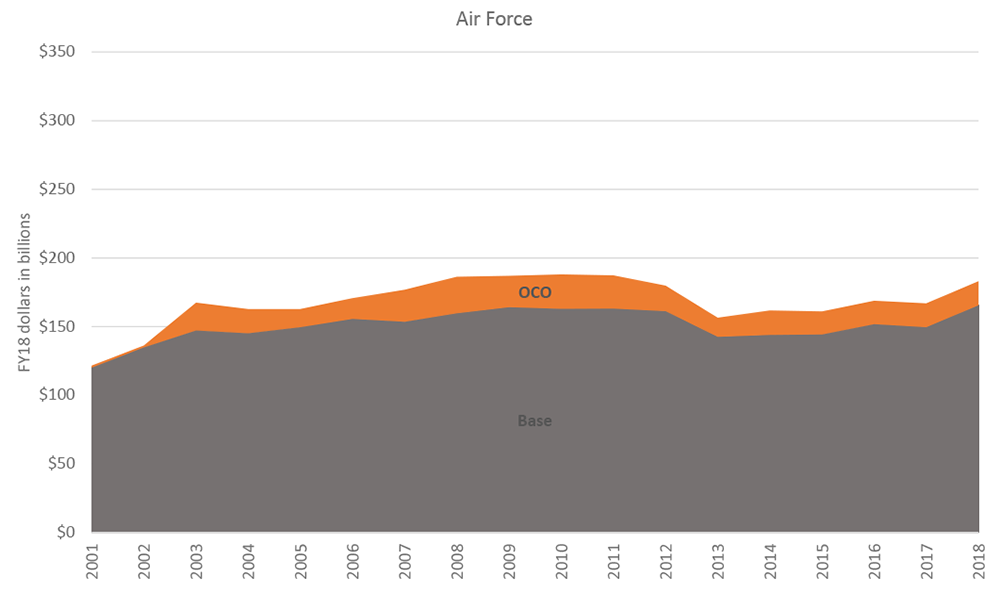

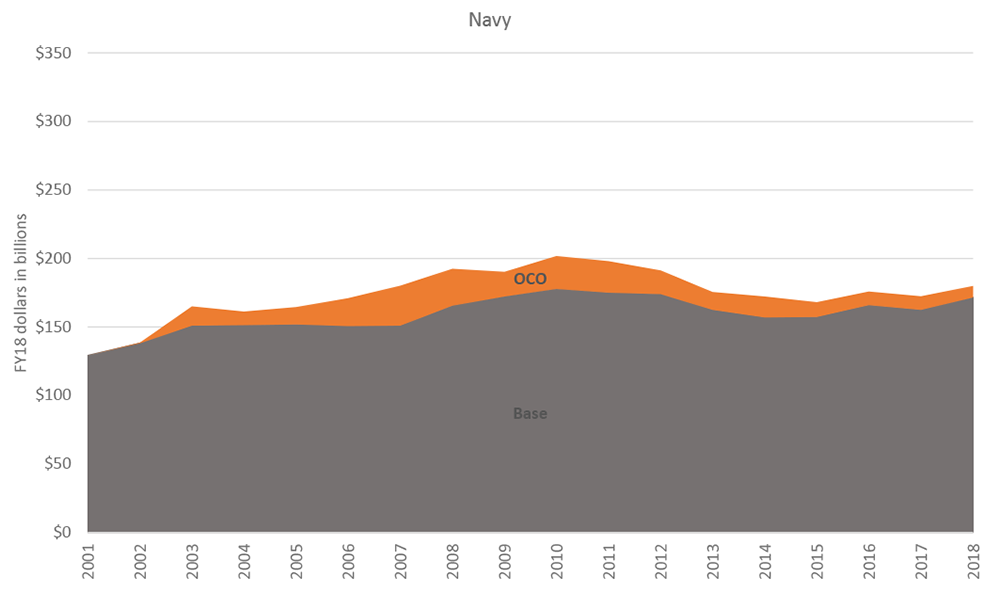

With the exception of the Army’s procurement spike during the Iraq and Afghanistan wars, principally for Mine-Resistant All-Purpose (MRAP) vehicles, Service procurement in the 2000s and 2010s was far below the Reagan-era average. From FY 1979 to FY 1992, Air Force procurement averaged $53.9 billion in FY 2018 dollars, whereas Navy procurement averaged $57.8 billion. Between FY 2003 and FY 2017, the Air Force’s procurement averaged $44.4 billion, $9.5 billion less annually than during the FY 1979–FY 1992 period; the Navy’s procurement averaged $46.8 billion, $11 billion less annually. This decade and a half of missing procurement is a major reason why the military is still relying on Regan-era systems for the bulk of the currently-fielded force structure, and why it faces difficult tradeoffs between maintaining and modernizing older equipment and purchasing new systems with the same scarce dollar.

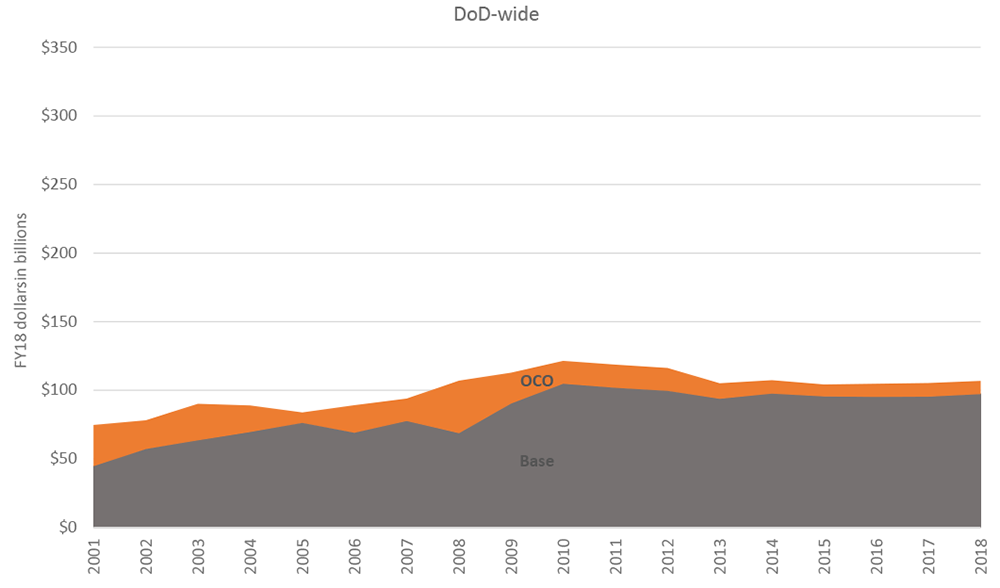

Figure 9-9: Procurement Funding by Service

Source: OUSD, FY 2018 Greenbook. Calculations by CSBA.

Procurement and RDT&E has increasingly been crowded out by long-term increases in O&M costs. A dollar of defense spending in FY 2018 buys less force structure than a dollar of defense spending did in FY 1983. Putting it another way, it has become costlier to maintain the same size force over time. Although modern systems are more capable than their predecessors, quantity is still required to perform many missions. This issue is highlighted by the strain that low ship numbers and high operational tempo have put on the surface Navy. Similarly, high operational tempo and maintenance and readiness challenges caused by a smaller, aging fleet are faced by U.S. combat air forces.

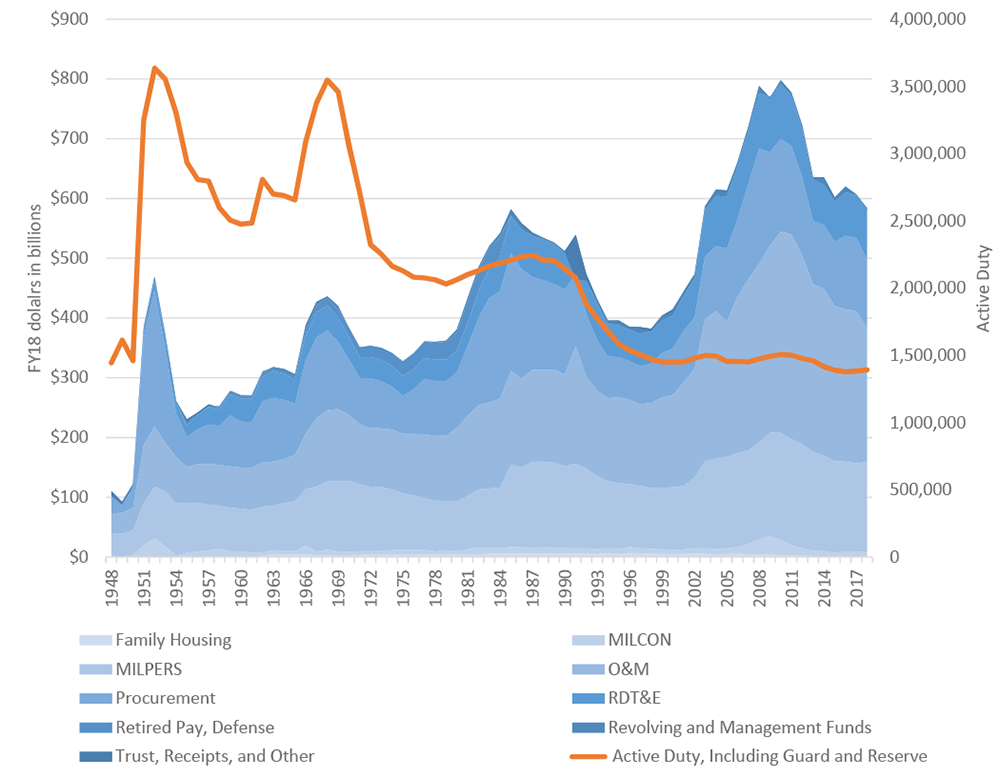

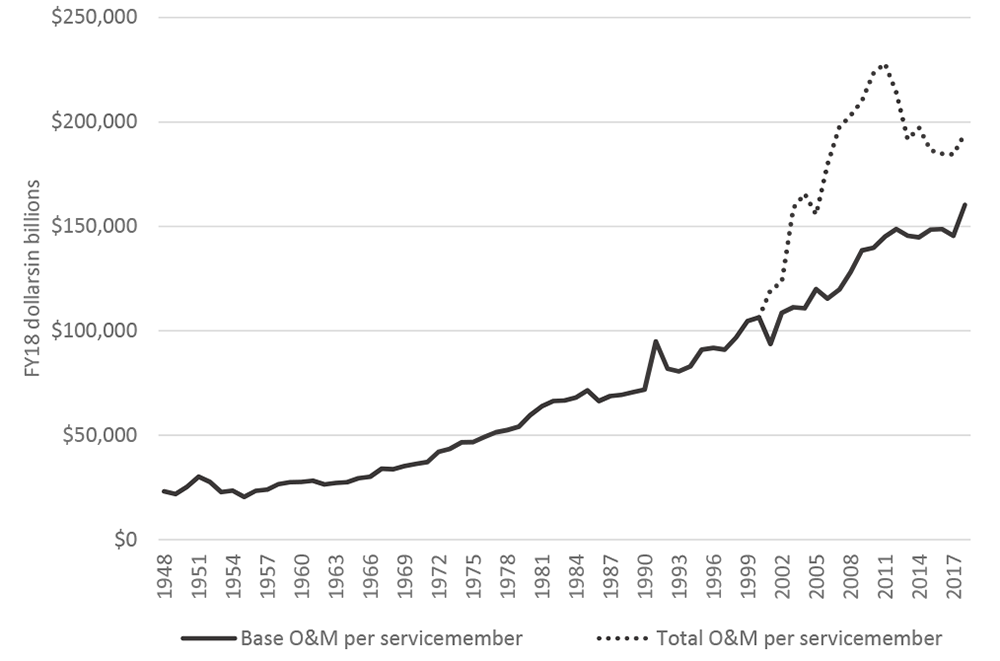

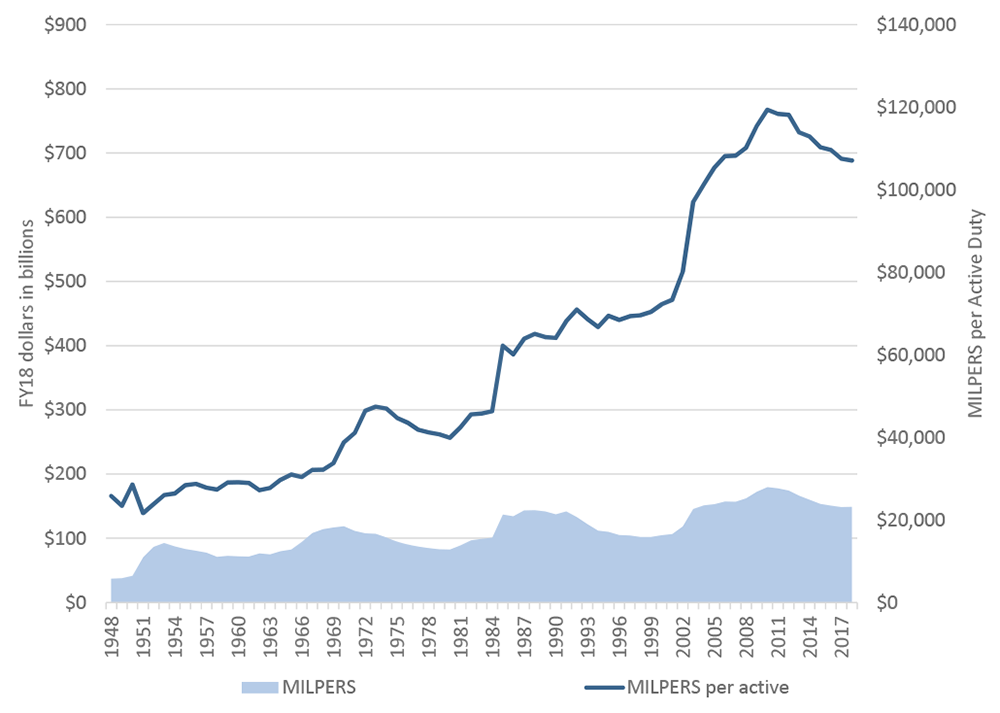

Spending on O&M and military personnel costs has grown in both real terms and as a percentage of the defense budget, even as the number of active-duty personnel has trended downward since the 1970s (see Figure 9-10). Since FY 1948, base budget O&M has grown by 2.7 percent annually over inflation. Since FY 2000, base budget O&M has grown by a CAGR of 2.1 percent, growing from $106,380 per active duty servicemember to $160,284 in FY 2018. Factoring O&M into war funding, total O&M has grown by a CAGR of 3.2 percent over inflation to $194,544 per active duty servicemember (see Figure 9-11). Similarly, the amount of military personnel funding per active duty servicemember or activated reservist has grown steadily as pay and benefits have increased. DoD now budgets $107,106 in military personnel funding for each active duty servicemember, a cumulative increase of 2.2 percent annually from $72,212 in FY 2000 (see Figure 9-12).

Figure 9-10: Defense Spending by Appropriations Title and Active Duty Servicemembers

Source: OUSD, FY 2018 Greenbook. Calculations by CSBA.

Figure 9-11: O&M Funding per Active Duty Servicemember

Source: OUSD, FY 2018 Greenbook. Calculations by CSBA.

Figure 9-12: Military Personnel Funding and Military Personnel Funding per Active Duty Servicemember

Source: OUSD, FY 2018 Greenbook. Calculations by CSBA.

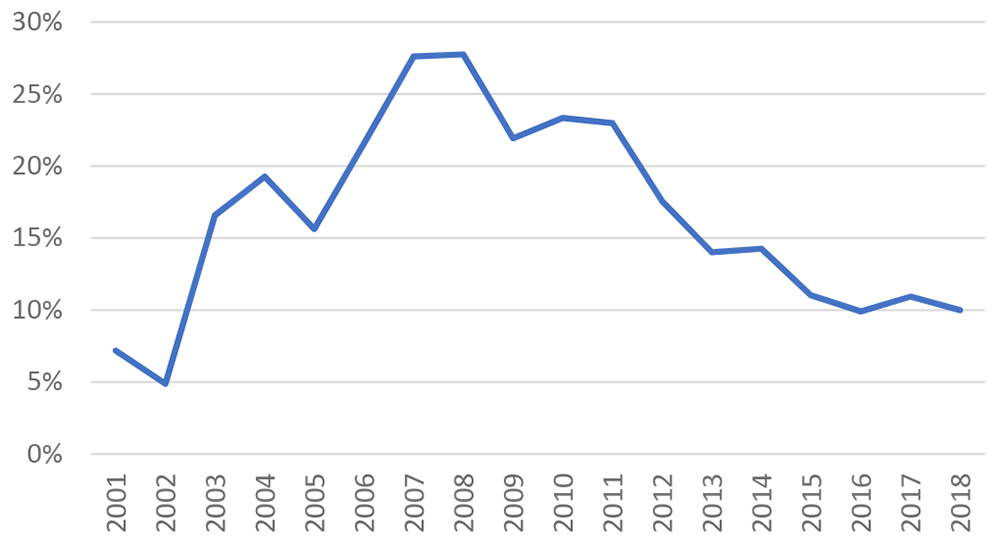

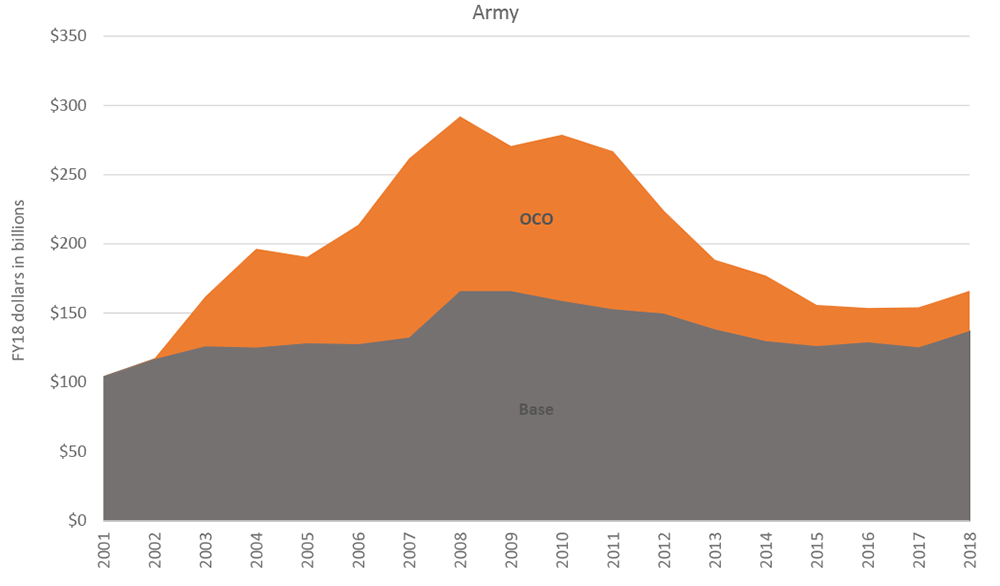

A final major difference between defense spending today and the FY 1979–FY 1985 defense buildup is the modern invention of OCO funding, which has become an essential component of the overall DoD budget. After the enactment of the Budget Control Act of 2011 and the imposition of caps on base discretionary national defense funding, but not on “emergency” funding, OCO has functioned as a safety valve for the overall DoD budget. At $64.6 billion, the FY 2018 request for funding of ongoing military operations is about 10 percent of the total DoD request for $647 billion. The overall level of OCO funding has declined by two thirds between the FY 2008 peak of $218 billion and the FY 2015 level of $66 billion, but has remained consistent at between $61.2 and $66.2 billion since then. Overall, war funding comprises a much smaller share of the total DoD budget than it did during the height of the wars in Iraq and Afghanistan. In FY 2007 and FY 2008, war funding accounted for 28 percent of the total discretionary DoD budget, but it has stabilized at about 10 percent of total discretionary DoD funding since FY 2015 (see Figure 9-13). The Services rely on OCO funding to different degrees. OCO makes up 17 percent of the Army’s total FY 2018 budget request, higher than any of the other Services, but a decline from FY 2007, when OCO made up 49 percent of the Army’s total budget. OCO accounts for 10 percent of the Air Force’s FY 2018 request, a relatively steady proportion since FY 2012. The Navy is the Service that is least reliant on OCO funding; it accounts for just 5 percent of the Navy’s FY 2018 request, down from 16 percent in FY 2007. Nine percent of the FY 2018 defense-wide spending is for OCO funds, down from 36 percent in FY 2008 (see Figure 9-14). According to estimates by the Government Accountability Office (GAO) and senior defense officials, approximately $20–30 billion of expenses properly considered base budget expenses are funded out of the OCO accounts. GAO has recommended that DoD revise the outdated 2010 Office of Management and Budget criteria for determining which defense costs can properly be considered OCO, potentially limiting the amount of base budget costs that can be funded via OCO.[7] However, shifting the full $20–30 billion enduring costs currently paid for through OCO back to the base budget would strain base Service budgets further.

Figure 9-13: OCO As a Proportion of Total Discretionary DOD Budget

Source: OUSD, FY 2018 Greenbook. Calculations by CSBA.

Figure 9-14: OCO As a Proportion of Service Budgets

Source: OMB, Historical Tables, Budget of the United States Government, Fiscal Year 2018, Table 1.3. Calculations by CSBA.

One of the most difficult balancing acts in the coming years will be between sustaining current operations while investing in the capabilities and technologies needed to deter, and if necessary fight and win, future wars. Key military challenges and competitions—predominantly countering Russian and Chinese anti-access and area-denial (A2/AD) capabilities, but including the proliferation of precision strike capabilities and the contestation of space and the electromagnetic spectrum—will play an important role in shaping warfare in the coming decades, particularly in how the military fights and what capabilities DoD will need to invest in. Maintaining the ability to operate in an environment where adversaries are capable of launching dense salvos of precision guided weapons requires a shift away from expensive long-range interceptors and toward both kinetic and non-kinetic short-range air and missile defense systems, battle management and fire control systems as well as electronic warfare systems to deceive and degrade adversary capabilities. A2/AD capabilities will put a premium on being able to operate and deliver strikes over longer ranges. Developing networked cross-domain sensing, targeting, and striking capabilities across the joint force will require investment in C4ISR, electronic warfare, sensors, and long-range strike weapons. Operating in more highly contested environments, much different from the largely permissive environments of the past decade and a half of conflict, places a premium on systems that are either low-observable (for high-value systems) or unmanned expendable systems.[8] At the same time, many of the missions U.S. forces conduct today, and are likely to continue conducting in the future, occur in more permissive environments where these advanced capabilities may not be needed, sparking discussion on the right high-low mix of capabilities. Additionally, today’s military is facing capacity challenges, with the current operational tempo straining the Services. However, adding additional end strength, planes, and ships to relieve the operational tempo burdens would also require substantial additional funding.

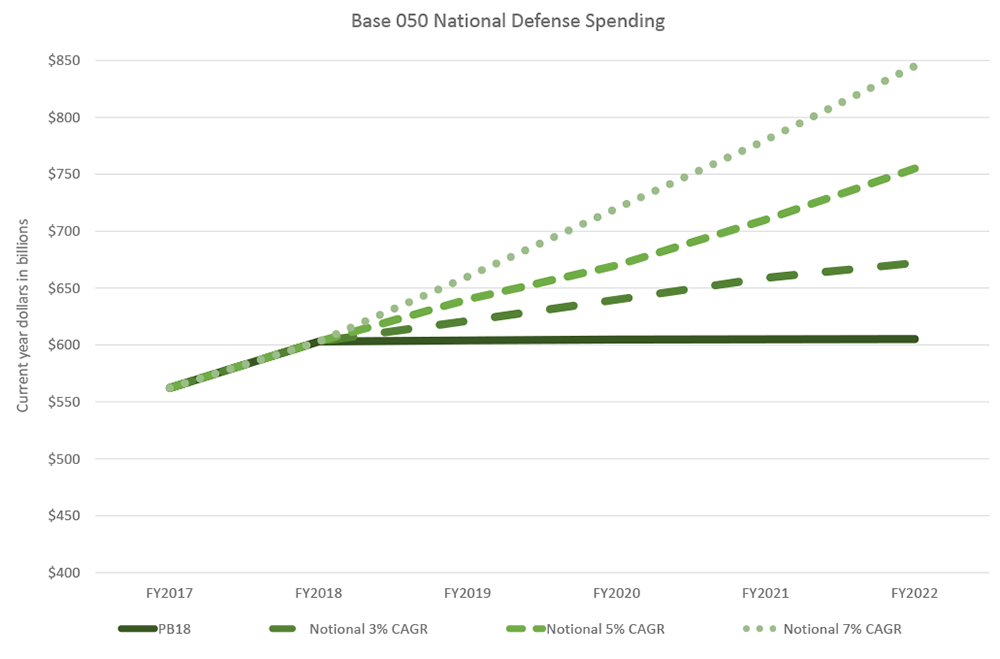

Senior Pentagon and military leaders, including Secretary Mattis, General Dunford, and the chiefs and vice chiefs of staff of each of the military Services have forcefully argued for more defense spending beyond FY 2018 in order to invest in the military capacity and capabilities needed now and for the future. Just as important, they have emphasized that the Pentagon needs stable, predictable, long-term funding.[9] At a 3 percent CAGR, base national defense spending would reach about $670 billion in FY 2022. At 5 percent, it would reach about $755 billion, and at 7 percent, it would reach $845 billion. Those spending levels would be between 20 and 50 percent higher than the FY 2017 levels. Notably, General Dunford testified that 3–7 percent annual growth would be sufficient for necessary capability investments, but insufficient to increase the Services’ force structure or end strength. The extant tensions between investing in capacity today vs. high-end capabilities for tomorrow will only grow more acute if the Congress is unable to bridge their sharp differences on fiscal policy and defense and non-defense spending to eliminate the BCA caps. Although it invests in improved readiness via increased training funding, maintenance funding, and healthier spare parts stockpiles and amps up investments in RDT&E, the FY 2018 budget continues to straddle this divide, postponing anticipated investments in capacity until FY 2019 and beyond.

Figure 9-15: Notional 3%, 5%, and 7% Annual Increases in Defense Spending Above FY18 Request Levels

Source: Office of Management and Budget, FY 2018 Budget, “Table 25.1, Net Budget Authority by Function, Category and Program.” Calculations by CSBA.

ABOUT THE AUTHOR

Katherine Blakeley is a Research Fellow at the Center for Strategic and Budgetary Assessments. Prior to joining CSBA, Ms. Blakeley worked as a defense policy analyst at the Congressional Research Service and the Center for American Progress. She is completing her Ph.D. in Political Science from the University of California, Santa Cruz, where she received her M.A. Her academic research examines Congressional defense policymaking.

ABOUT THE CENTER FOR STRATEGIC AND BUDGETARY ASSESSMENTS (CSBA)

The Center for Strategic and Budgetary Assessments is an independent, nonpartisan policy research institute established to promote innovative thinking and debate about national security strategy and investment options. CSBA’s analysis focuses on key questions related to existing and emerging threats to U.S. national security, and its goal is to enable policymakers to make informed decisions on matters of strategy, security policy, and resource allocation.

NOTES

[1] Joe Gould, “Thornberry Wins Pledge to Grow DOD Budgets, But Will It Stick?” Defense News, June 27, 2017, available at https://www.defensenews.com/congress/budget/2017/06/27/thornberry-wins-pledge-to-grow-dod-budgets-but-will-it-stick/.

[2] Tony Bertuca, “Dunford: DOD Needs Between 3 Percent and 7 Percent Growth Annually,” Inside Defense, September 26, 2017, available at https://insidedefense.com/daily-news/dunford-dod-needs-between-3-percent-and-7-percent-growth-annually.

[3] This defense investor sentiment was relayed in email newsletters from Capital Alpha Partners.

[4] For an excellent overview of the evolving national security analysis of shifts in the international strategic landscape and security environment over the past several years, see Ronald O’Rourke, A Shift in the International Security Environment: Potential Implications for Defense, R43838 (Washington, DC: Congressional Research Service, August 16, 2017), Appendix A, “Articles on Shift to New International Security Environment.”

[5] The 1981 tax cuts were enacted by the Economic Recovery Tax Act of 1981 ,P.L. 97-34.

[6] Gallup News, “Military and National Defense,” polling conducted February 1–5, 2017, available at http://news.gallup.com/poll/1666/military-national-defense.aspx.

[7] Government Accountability Office (GAO), Overseas Contingency Operations: OMB and DOD Should Revise the Criteria for Determining Eligible Costs and Identify the Costs Likely to Endure Long Term, GAO-17-68, report to congressional requesters (Washington, DC: GAO, January 2017), available at http://www.gao.gov/assets/690/682158.pdf.

[8] For discussion of strategic approaches in the evolving international security landscape and future military operational challenges, concepts, and capabilities, see selected recent CSBA reports Preserving the Balance: A U.S. Eurasia Defense Strategy, by Andrew F. Krepinevich; Avoiding a Strategy of Bluff: The Crisis of American Military Primacy, by Hal Brands and Eric Edelman; Dealing with Allies in Decline: Alliance Management and U.S. Strategy in an Era of Global Power Shifts, by Hal Brands, and Extended Deterrence in the Second Nuclear Age, by Evan Montgomery. For discussions of future military competitions and U.S. operational concepts and capabilities, see Restoring American Seapower: A New Fleet Architecture for the U.S. Navy, by Bryan Clark et al.; Wining the Salvo Competition: Rebalancing America’s Air and Missile Defenses, by Mark Gunzinger and Bryan Clark; Trends in Air-to-Air Combat: Implications for Future Air Superiority, by John Stillion; Winning the Airwaves: Regaining America’s Dominance in the Electromagnetic Spectrum, by Bryan Clark and Mark Gunzinger; What it Takes to Win: Succeeding in 21st Century Battle Network Competitions, by John Stillion and Bryan Clark; and Toward a New Offset Strategy: Exploiting U.S. Long-Term Advantages to Restore U.S. Global Power Projection Capability, by Robert Martinage.

[9] General Daniel Allyn, Vice Chief of Staff United States Army; Admiral William Fm. Moran, Vice Chief of Naval Operations; General Glenn Walters, Assistant Commandant of the Marine Corps; and General Stephen W. Wilson, Vice Chief of Staff of the Air Force, “Current State of Readiness of the U.S. Armed Forces,” Statements before the Senate Armed Services Committee, Subcommittee on Readiness and Management, February 8, 2017; and General Mark Milley, Chief of Staff United States Army; Admiral John M. Richardson, Chief of Naval Operations; General Robert B. Neller, Commandant of the Marine Corps; and General David L. Goldfein, Chief of Staff of the Air Force, “Impacts of a Year-Long Continuing Resolution,” Statements before the House Armed Services Committee, April 5, 2017.